How to Do a Backdoor Roth IRA

I started a Backdoor Roth IRA in 2025, and it was surprisingly simple.

Now, I am no financial expert (and, of course, this is not financial advice) - so it took me some time to learn this. Having said that, here's what I've learned.

But first, before we delve into how to do a Backdoor Roth IRA, let’s talk about why to do a Backdoor Roth IRA.

What is a Backdoor Roth IRA?

A Backdoor Roth IRA allows high-earners to contribute to a Roth IRA (and thus, benefit from the tax advantages of a Roth IRA), whereas otherwise they would be unable to do so.

In 2025, single-contributors must have earned less than $150,000 to contribute to a Roth IRA. The contribution limit was $7,000, and is increasing to $7,500 in 2026.

Meaning, if you earn more than $150,000, you cannot contribute directly to a Roth IRA. However, you can still contribute indirectly, using the Backdoor Roth IRA pathway.

Why do a Backdoor Roth IRA?

A Roth IRA is a retirement savings account that accepts after-tax money. While that does mean no upfront tax deduction (such as with a 401(k), it also means that your qualified withdrawals in retirement are completely tax-free, making it ideal if you expect to be in a higher tax bracket later. And even if you don’t expect to be in a higher tax bracket later, it allows for tax-free growth of your investments during earning years. That is, compared to a taxable brokerage account, with a Roth IRA you won’t pay taxes on interest, dividends, and capital gains.

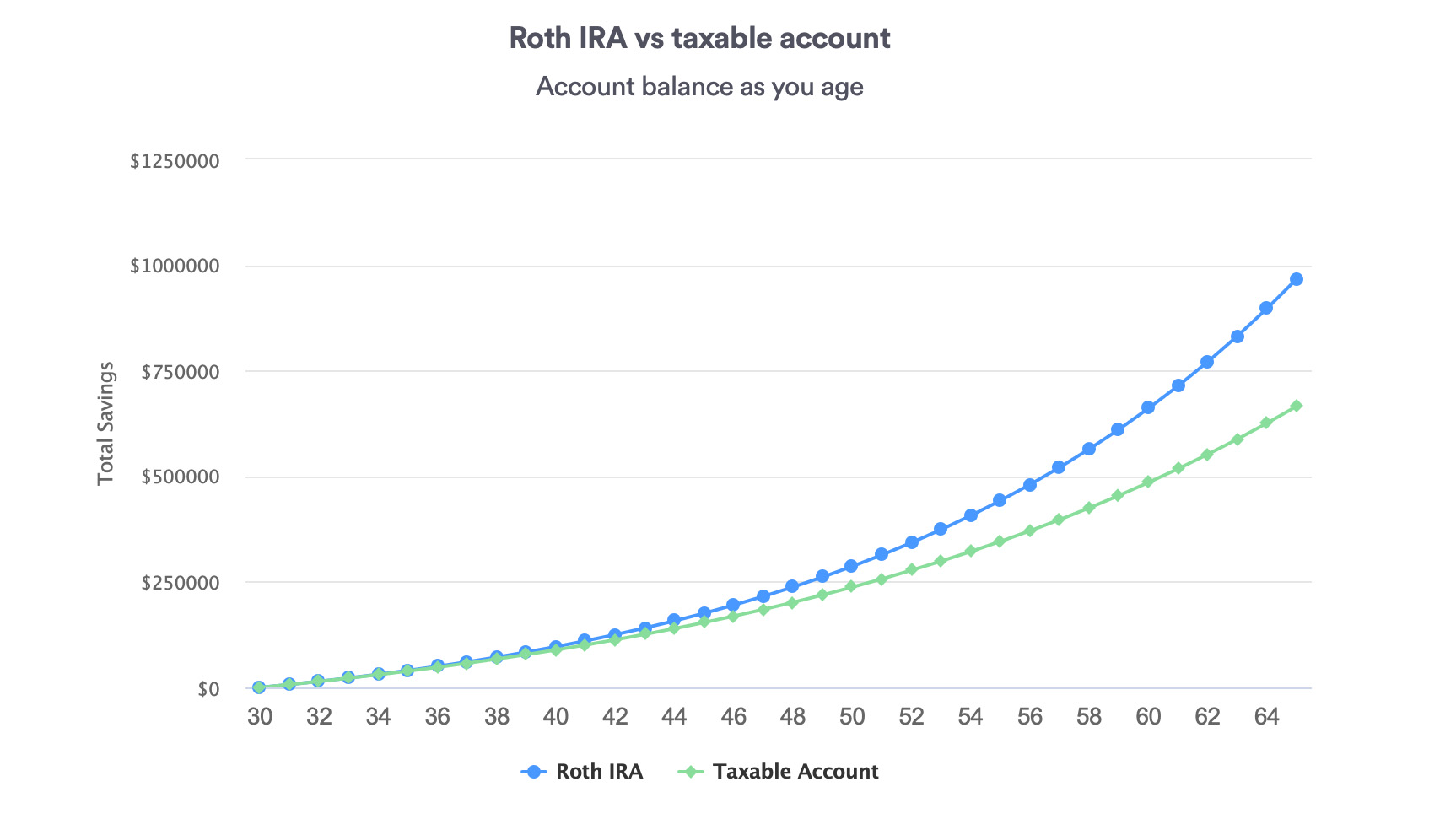

Here’s what that means in cold, hard numbers according to Bankrate.com:

For a 30-year-old single-earner, contributing the current maximum to a Roth IRA, he or she would earn $967, 658 in retirement using a Roth IRA, compared to just $665, 971 using a taxable brokerage account. Or, a difference of $301,687.

How to do a Backdoor Roth IRA

Convinced? OK then, here’s how to do it.

(Keep in mind, most residents and fellows can (and I think, should) just contribute to a Roth IRA directly. There is no need to complicate things with a Backdoor Roth IRA process.)

A Backdoor Roth IRA transfer involves, essentially, two steps:

- Add money to a Traditional IRA

- Transfer that money to a Roth IRA

How to do a Backdoor Roth IRA (in more detail)

Here’s how to do it, in a bit more detail:

- Contribute to a Traditional IRA (keep in mind, the contribution limits change over time; in 2025, it was $7,000)

- Don’t invest the contribution! Let its in cash. We don’t want our contributions earning interest

- The next day, transfer the money from the Traditional IRA to the Roth IRA

- Once it clears, go ahead and Invest the money into your investment of choice

- Come tax season, remember to fill out Form 8606 on your tax returns

And then one additional word of caution: Avoid the pro-rata rule.

The pro-rata rule essentially treats all of one’s IRAs as a single account, and in doing so blends the taxable percentage of any transfer based on its proportion within the entire account. What that means, in the simplest terms, is that if you have an existing IRA (which contains pre-tax money), you will pay taxes on the Backdoor Roth IRA conversion (even if it was contributed with post-tax money).

For example, if the existing IRA contains $93,000 in pre-tax money, and you contributbe $7,000 for the Backdoor Roth IRA conversion, and then transfer that contribution, the IRS will still consider that $7,000 taxable. How taxable? Well...

$7,000 (Backdoor Roth IRA) / $100,000 (total IRA) = 7% non-taxable (or, 93% taxable)

$7,000 x 0.93 (taxable percentage) = $6,510 of the transfer is taxable.

So, 93% taxable, based upon its proportion within the overall IRA. Having 93% of your contribution taxed more or less eliminates the benefit of the Backdoor Roth IRA in the first place.

However, if we have $0 in the IRA at the time of transfer, then all or 100% of the conversion is post-tax and thus non-taxable income, and we will pay no taxes on the transferred amount.

If you do have an existing IRA, you can get rid of these accounts in the following ways:

- Withdrawing the money (not recommended)

- Roll the money over into an alternative investment account (e.g., a 401(k) , 403(b), or individual 401(k) (much better)

And possibly a few others. I used options number two (roll the money over into an alternative investment account), which is likely the best option for most people.

The downsides of a Backdoor Roth IRA are, of course, more paperwork, which makes for a slightly harder tax return season. But the benefits? Potentially over $300,000.